Your profit margin is a metric that should always be on your radar, and for good reason: it answers critical questions about your business, like whether or not you’re making money or if you’re pricing your products correctly.

It’s important to note, though, that your profit margin isn’t just something you should measure; it’s a metric that you should continuously improve. As author Doug Hall said, “If your profit margins aren’t rising, chances are your company isn’t thriving.”

To help you better understand how to increase profit margins in your business, we’ve put together some tips and expert advice on retail profitability. You’ll learn the following:

- What gross profit is and how to calculate it

- Defining gross profit margin and how to calculate it

- What net profit is and how to calculate it

- The factors that contribute to profit margin

- What the ideal profit margin is

- 20 actionable ways to increase profit margins

Let’s dive in!

Prepare your business for the future of commerce

Download our free playbook and learn how to sell on different channels, boost loyalty and increase foot traffic with technology.

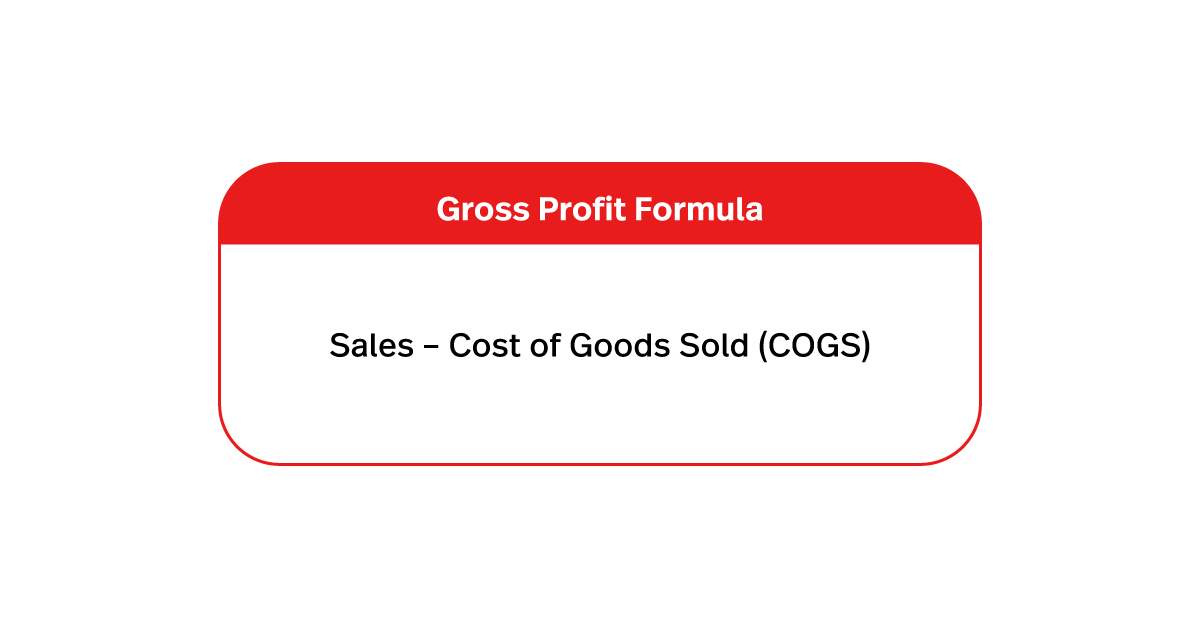

What is gross profit?

Gross profit is your total revenue minus the cost of generating that revenue. Simply put, gross profit is your sales minus the cost of goods sold (COGS). Your gross profit tells you how much money your business has before paying for other expenses like payroll, marketing, utilities, etc.

Gross profit formula

Your gross profit is calculated by subtracting the cost of goods sold from your sales. Expressed as a formula, it looks like this:

Understanding gross profit

Let’s say that Johnny’s Bikes sold $20,000 worth of Bike #1 in one month. Their inventory cost them $10,000. Bike #1’s gross profit is $10,000.

In that same month, Johnny’s Bikes sold $15,000 worth of Bike #2 and its COGS was only $2,000. Bike #2’s gross profit is $13,000.

Although Bike #2 sold for less than Bike #1, its gross profit is higher, therefore the bike is more profitable to sell.

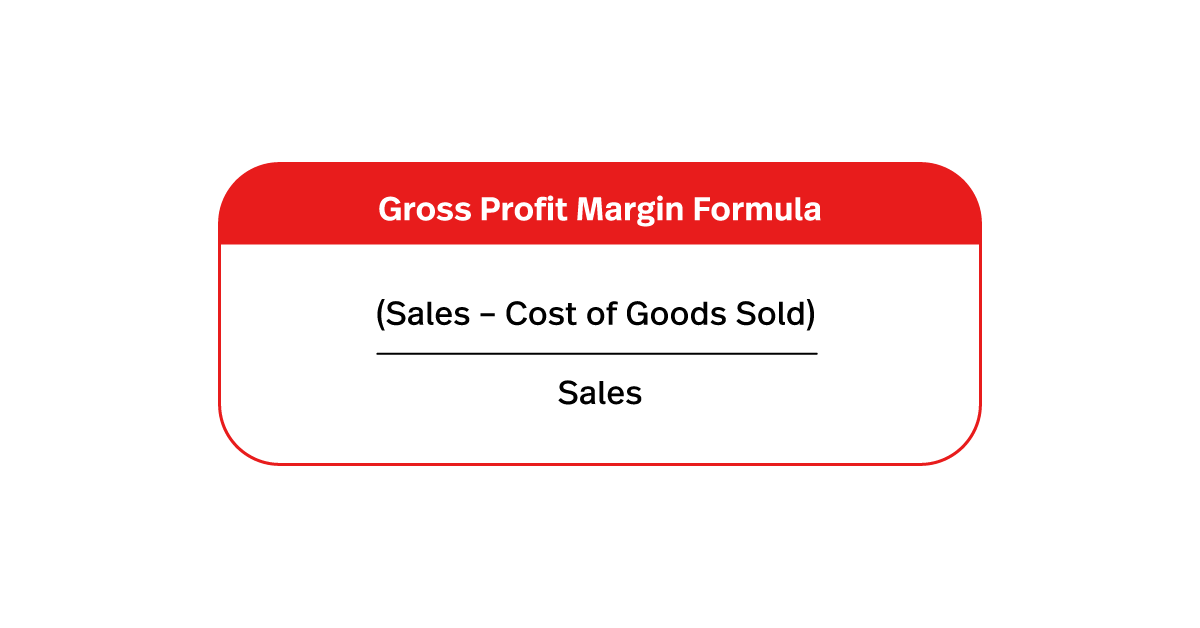

What is gross profit margin?

Gross profit margin is when you express gross profit as a percentage. The higher the percentage, the more profitable an item is for a business to sell.

Gross profit margin applies to a specific product a business sells. Calculating gross profit margin enables businesses to set prices that make selling the product worthwhile.

Gross profit margin formula

Your gross profit margin is calculated by first subtracting the cost of goods sold from your sales, then dividing that amount by sales. Expressed as a formula, it looks like this:

Understanding gross profit margin

Taking the same example as we did for gross profit, let’s explore the gross profit margin of Bike #1 and Bike #2 at Johnny’s Bikes.

Bike #1 sold for $20,000 and its gross profit was $10,000.

Gross profit margin = 10,000 / $20,000

Gross profit margin = 0.5

Gross profit margin = 50%

Bike #1’s gross profit margin is 50%.

Bike #2 sold for $15,000 and its gross profit was $13,000.

Gross profit margin = 15,000 / 13,000

Gross profit margin = 1.15

Gross profit margin = 115%

Bike 2’s gross profit margin is 115%. Since its cost of goods sold is less than Bike #1, it’s more worthwhile for Johnny’s Bikes to sell Bike #2 than it is Bike #1 because they’re making more profit on each sale.

What is net profit margin?

Let’s say you wanted to express your entire business’s profitability rather than just one product; that’s your net profit margin. A business’s net profit margin is expressed as a percentage.

The higher the percentage, the more profitable the business is. A low net profit margin is a signal that there are issues impacting your business’s profitability potential, from high expenses (rent, utilities, labor, etc), issues with productivity or even management issues.

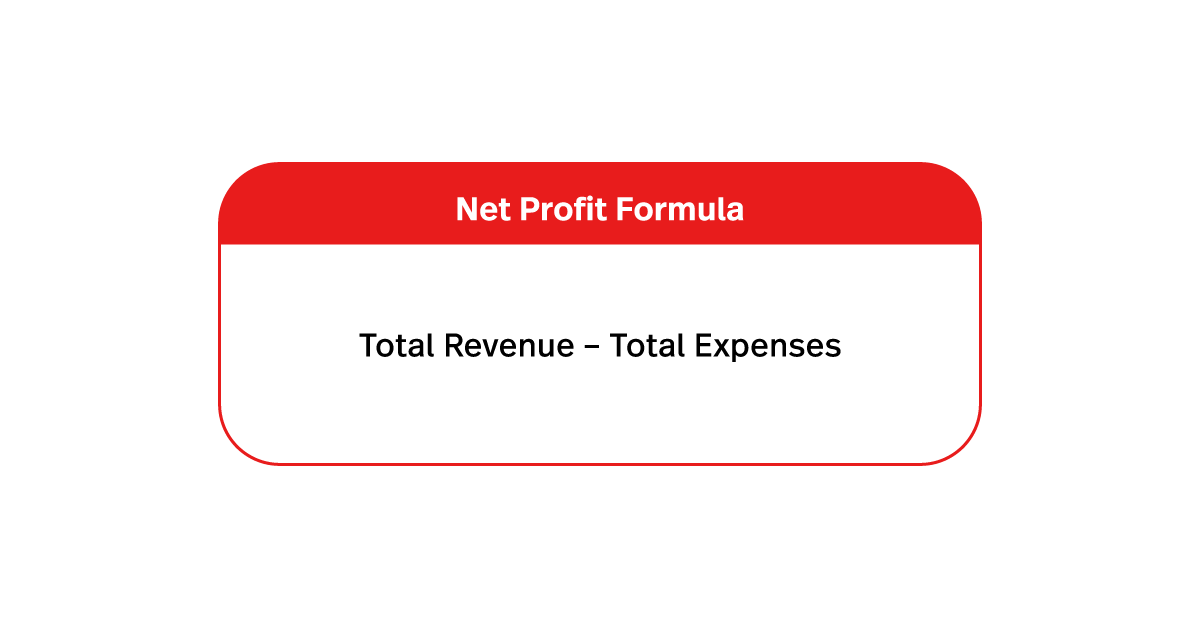

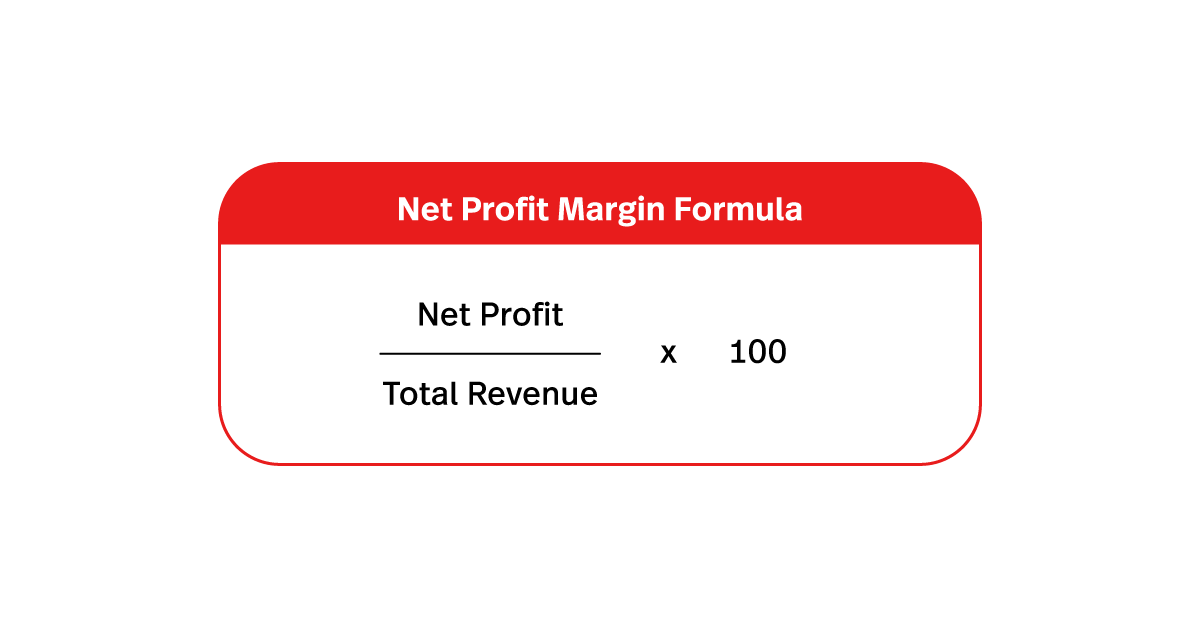

Net profit formula

To calculate net profit margin, you first need to find your net profit by subtracting your total expenses from your total revenue.

Net profit margin formula

Next, divide your net profit into your total revenue and multiply the result by 100 to express the value as a percentage.

Understanding net profit margin

Let’s say Johnny’s Bikes’ gross sales are $500,000 and their total expenses are $250,000. Their net profit would be $250,000.

Net profit = $500,000 – $250,000

Net profit = $250,000

To express your business’s net profit as a percentage, do the following:

Net profit margin = ($250,000 / $500,000) x 100

Net profit margin = 0.5 x 100

Net profit margin = 50%

What contributes to profit margins?

There are many things that factor into a retailer’s profit margins, including markdowns and promotions.

When you sell an item for less than your initial markup (IMU), you’re effectively lowering your profit margin on that item. That’s why having the right markdown strategy is so important. You never want to arbitrarily attribute a discount to a product; always pinpoint a retail price that will be both interesting for deal-hunters and profitable for your business.

Your point of sale system can also help. One of the main reasons retailers discount products is to liquidate old inventory that wasn’t selling at full price. A retail POS system with inventory management capabilities will keep you from ordering too many units of a product, preventing you from having to discount its price to get rid of excess inventory in the first place.

What is the ideal profit margin?

Profit margins vary greatly depending on a retailer’s sub-sector and what products or services they sell.

For instance, a fashion and apparel store’s profit margins will vary greatly based on what type of clothing it sells (is it fast fashion, mid-level or luxury goods?). If we were to compare the profit margins of a clothing store to that of a hand-made furniture store, they would vary greatly even if their respective profit margins are healthy for their respective sub-sector or niche.

Based on our data, we found that the average gross profit margin in retail is 53.33%. When comparing profit data across multiple industries, we found that beverage manufacturers, jewelry stores, and cosmetics had some of the highest profit margins, with 65.74%, 62.53%, and 58.14%, respectively. Meanwhile, alcoholic beverages, sporting goods stores, and electronics had some of the lowest margins at with 35.64%, 41.46%, and 43.29% respectively.

20 ways to increase your profit margins

Now that you know what gross profit is and how to use it to attribute a product’s monetary value for your business, let’s look at eight tried-and-true ways on how to increase profit margins in retail.

- Bring your brick-and-mortar store online

- Avoid markdowns by improving your inventory purchasing

- Plan ahead for each season

- Find ways to reduce operating expenses

- Increase your average transaction value (ATV)

- Elevate your brand and increase the perceived value of your merchandise

- Increase your prices

- Optimize vendor relationships

- If you must discount your products, be smart about it

- Inspire your staff to do more

- Get more sales from your existing customers

- Leverage technology for efficient operations

- Manage customer relationships effectively

- Maximize online sales opportunities

- Practice sustainability for long-term profitability

- Analyze market trends for strategic decisions

- Train and motivate employees

- Optimize store layout and design

- Implement loyalty programs and incentives

- Build a strong online presence

1. Bring your brick and mortar store online

It’s imperative that your customers are able to find your retail business online.

This can be as simple as creating a Google My Business profile to help more local customers find your store either through Google Search or Google Maps. According to Google, 88% of people that search for a local business online either call or visit that business within 24 hours. Setting up a GMB profile helps businesses convert online visibility into in-store transactions.

If you want to take it a step further, consider launching an online store. While getting started may seem like a daunting task, you can always start small and work your way up as you have time and resources.

Even a basic (but well-designed) website that features your business name, location and contact information is beneficial for helping customers find your store. But the real benefit of setting up an online store is creating a secondary sales channel to complement brick-and-mortar sales.

With Lightspeed eCom, you can build a transactional website using handy templates, sync your physical store’s inventory with your online store and manage both from the same backend.

An online store can increase your exposure and sales while costing far less than opening a second physical location.

Key takeaways:

- Set up a GMB profile to increase your retail store’s visibility and convert that into in-store sales.

- Create a transactional online store to increase sales at a lower cost than if you were to open a second brick-and-mortar location.

2. Avoid markdowns by improving your inventory purchasing

Whenever you lower the price of an item, you’re also lowering that item’s profit margins. That’s why it’s best to avoid markdowns whenever possible.

The most effective way to avoid markdowns is to improve your inventory management, the merchandise you have on hand, the products that sell quickly at full price and the ones that don’t. That information (which you can typically find in your POS system’s sales reports) will help you decide which products to stock up on and how much to buy to fulfill customer demand, prevent overstocking and avoid the need for markdowns and promotions altogether.

Key takeaways:

- Use your sales and inventory data to get a clear understanding of how much inventory you have, which products sell at full price and what doesn’t sell unless marked-down (or doesn’t sell at all).

- Leverage those insights when purchasing inventory to assure that buying products that sell at full price and not over-stocking either.

3. Plan ahead for each season

Most retail businesses have a season where their sales peak. A retailer’s peak season will vary based on their sector, product-type and their location. Even then, most retailers in the US will experience a fluctuation in sales from one month to another.

Retailers should get into the habit of looking at their annual sales reports, broken down month-by-month. Which months do they make the most sales in? Does that pattern persist year after year?

Use those patterns when planning your seasonal inventory purchasing. If you notice that you sell a higher volume of certain product types in a given season, consider purchasing more units of that item to capitalize on its seasonality and maximize sales.

A secondary benefit to planning your seasonal inventory ahead is that suppliers may offer discounts for advanced or bulk orders. You may be able to lower that item’s COGS, maintain its retail price and maximize that item’s gross profit.

Key takeaways:

- Look at your annual sales reports broken down month-by-month and take note of any patterns.

- Use that data to plan what seasonal inventory you will carry in advance. Suppliers may offer discounts on purchase orders submitted in advance.

4. Find ways to reduce operational expenses

Krista Fabregas, a retail analyst at FitSmallBusiness, suggests that retailers find ways to streamline their operations as a way to increase profit margins.

There are several key areas where a retailer can reduce operational costs. For starters, look at labor costs and avoid overstaffing. Next, look at other costs like your product packaging, shopping bags and even your store lighting. Are there any costs that can be reduced? In the case of lighting, it may be worthwhile to invest in energy-efficient commercial lighting.

Another way to reduce operational costs is by streamlining productivity. Are there certain repetitive tasks that are taking up chunks of you and your staff’s time? A usual culprit is anything to do with data entry.

The good news? Most time-consuming data entry tasks can be automated. For example, rather than manually transferring sales data from your point of sale system to your accounting software, consider using a two-way integration like Lightspeed Accounting, which automatically pushes information from one system to the other. Spend less time punching in numbers (or avoid paying someone to do that task for you) and benefit from accurate bookkeeping.

Key takeaways:

- Find places where you can lower your overhead spending without sacrificing the quality of your customer experience.

- Automate time-consuming, repetitive tasks to save time and lower your expenses.

- If you use Lightspeed, visit our integrations page to find tools that help you automate tasks.

5. Increase your average transaction value (ATV)

Increasing your store’s average transaction value (ATV) is both an excellent and achievable way to increase profits. Retail is an inherently social activity and, although technology helps merchants serve customers, nothing can replace the connection between an empathic and informative (but not pushy) sales associate and their customer.

But how can you use social interactions to boost ATV?

Teach your sales associates the art of suggestive selling. Once a customer is in your store, it’s on your sales associates to build a rapport, listen intently to their needs and find products that fulfill those needs.

Your store layout has an impact on in-store sales, too.

How you promote and display your products in-store, known as visual merchandising, can help customers find what they’re looking for, discover related products and make a purchase. Point of sale marketing (placing low-investment products near the checkout) is another tactic retailers use to increase impulse purchases and a customer’s transaction value.

Key takeaways:

- Teach your sales associates the art of suggestive selling to help them close more sales without coming off as pushy.

- Assure that your visual merchandising helps customers find what they’re looking for, discover related products and add more items to their transaction without the help of a sales associate.

6. Elevate your brand and increase the perceived value of your merchandise

It’s interesting to see that cosmetics retailers have some of the best margins in retail. According to experts, one reason behind this is the fact that beauty and cosmetics brands excel at creating personal and emotional connections with customers.

“Beauty is a category on fire… The price value equation is quite good, cosmetics make people feel better about themselves and foster strong customer loyalty, and the merchandising creates a sense of exploration,” says Laura Heller, former editor at Retail Dive.

She continues, “The product category creates a kind of personal connection with shoppers, unlike many other consumer goods. The price value equation is quite good; cosmetics make people feel better about themselves and foster strong customer loyalty, and the merchandising creates a sense of exploration—something the off-price retailers have also done quite well. Depending on the brand, packaging, and marketing attached, the profit on each small item can be really high.”

Chris Guillot, founder of Merchant Method, offers a similar view, saying that “cosmetics brands do a great job with brand management, playing to their customer base at an emotional level—status and lifestyle.”

According to Guillot, “Retailers of all sizes and stages of growth can focus on their unique brand positioning as a way to differentiate from their competitors and increase perceived value.”

Key takeaways:

- Find ways to increase the perceived value of your brand. You can do this by focusing on the emotional and lifestyle values that your merchandise can offer.

- For example, can your products make people feel better about themselves? Can they elevate the lifestyle of your customers? Brands that are able to do these things can often charge a premium for their products.

7. Increase your prices

Raising your prices will enable you to make more money on each sale, thus widening your margins and improving your bottom line. Many retailers, however, balk at the prospect of increasing their prices out of fear that they’ll lose customers.

We wish we could give you hard and fast rules when it comes to pricing, but the fact is, this decision depends on each company’s products, margins, and customers. The best thing to do is to look into your own business, run the numbers, and figure out your pricing sweet spot.

On top of considering basic pricing components like your costs and margins, look at external factors such as competitor pricing, the state of the economy, and the price sensitivity of your customers.

And consider what types of customers you want to attract. Do you want to sell to shoppers who would take their business elsewhere just because they could get an item for less, or would you rather attract customers who don’t base their purchase decisions solely on price?

You’d be surprised to find that the majority of consumers (though this may vary from one industry to the next) may actually belong to the latter group. A 2023 report by PwC says 42% of customers would pay more for a positive experience.

Take all these things into consideration; do the math, and once you come up with a price increase, test it on a few select products then gauge customer reaction and sales from there. If the results are positive, roll out the increase across all your products.

Be creative with your price increases

You may also want to consider implementing creative or psychological tactics when coming up with your prices, to make them more appealing. You can, for instance, incorporate tiered pricing into your strategy.

Check out what shoe retailer Footzyfolds did. To combat cheaper knock-offs of its merchandise (they were selling them for $25, while Target had them for $10) the store decided to revamp its prices—but not in the way you might think.

Instead of lowering prices across the board, Footzyfolds introduced a high-end category for their products. With the new pricing format, they lowered the price of their everyday products to $20 a pair, but introduced a new “Lux” category for $30 a pair.

Owner Sarah Caplan told the New York Times that this move helped them increase profits. “We actually have had the most interest in our higher-priced shoes,” she said to the publication and reported that after launching the high-end line in the summer of 2010, they saw revenues increase by 100%.

Key takeaways:

- If it makes sense for your business, go ahead and raise your prices. Krista Fabregas recommends that you start with your top sellers. “Do you have a lot of competition, or do your products stand alone? If so, raise your prices on these products.”

- Be creative with your prices. Factor in psychology or use methods like tiered pricing.

8. Optimize vendor relationships

Earlier in this post, we discussed the importance of implementing smarter inventory management and purchasing practices. If you want to take things a step further, consider building stronger relationships by working more closely with them.

Engage in joint business planning

Daniel Duty, co-founder and CEO of Conlego, says that retailers should engage in joint business planning with vendors. “This is a collaborative tool whereby profit goals are agreed to, and initiatives are developed to help reach those goals. In other words, both sides help each other become more profitable,” he shares.

Reduce supply chain costs and inefficiencies

“The supply chain—or the process of getting a product from the factory to the store floor — is always full of inefficiencies and huge costs,” adds Daniel.

“Retailers should study their supply chain to figure out where there are unnecessary costs. For instance, shipping product in less than a full truckload is more costly than when it is full. Making many deliveries each week to a store is more expensive than just one. Retailers should ask their suppliers if they are doing anything that is adding to costs to the supply chain that could be stopped.”

It also helps to have a discussion with your vendors to see if there’s anything you can do to make things easier or more cost-effective.

That’s what photo digitization service ScanMyPhotos.com did. President and CEO Mitch Goldstone says that collaborating closely with their vendors enabled them to enhance their business processes. “We invite our vendors to think of us as a partner. The better we do, the better they do. The process is simple, just ask vendors to help improve your workflow.”

Goldstone shares that they even invited one of their vendors, the United States Postal Service, to visit their headquarters. “We asked them to study our entire shipping operation and the technology that drives our fulfillment services. Many, many elements we thought helped streamline the business were all wrong and the USPS marketing team became our best partner to reinvent everything.”

See if you can do the same thing in your business. Strengthen your relationships with vendors and determine how you can work better together. Doing so could help you identify ways to reduce product costs and operating expenses. Or, at the very least, it could improve your workflow and productivity.

Key takeaways:

- Have a collaborative relationship with your vendors. Engage in joint business planning and figure out how you can both improve profitability.

- Identify inefficiencies in your supply chain and find ways to reduce them.

9. If you must discount your products, be smart about it

While discounting typically goes against traditional advice on profitability, it could work to your advantage if you do it right.

For instance, you could provide tailored and personalized offers. Remember that not all customers are wired the same way. Some people may need a 20% off incentive to convert, while others don’t really require a lot of convincing.

Instead of killing your profits with large, one-size-fits-all offers, identify how big of a discount is necessary to convert each customer.

Timing is also critical. As M. Pope Anthony, president and buyer at Anthony’s Ladies Apparel, notes, “there is a fine line between too soon and too late. If you hold on to items too long, you will eventually have to sell them at a much deeper discount.”

Good historical information and experience are crucial. Being overstocked on old, undesirable inventory will tie up your dollars and prevent you from buying new products. Eventually, your volume will decline, rendering you with fewer margin dollars.

Key takeaways:

- Personalize offers so you’re not giving away too big of a discount to people who would convert at a lower threshold.

- Get your timing right and test different types of promotions to see which ones are really making you money.

10. Inspire your staff to do more

One way to boost your profits is to increase the output of your existing staff. No matter what type of store you’re running, there’s a good chance that your employees aren’t being as productive as they could be—and that’s not necessarily their fault.

According to the Harvard Business Review, companies lose over 20% of their productive capacity to organizational drag — “the structures and processes that consume valuable time and prevent people from getting things done.”

As such, it’s important that you evaluate your store processes to ensure that they’re not slowing people down. The key is to come up with procedures that can easily be replicated and implemented by your staff even when you’re not around. (Hint: if you have the right POS and retail management system, you’re off to a great start!)

Once you’ve tightened up your processes, you can work on empowering and training your team to level up their game. There’s no one right way to do this, as each retailer is different. But here are a few ideas:

- Set the right sales targets and motivate your team to meet (and beat) those goals.

- Identify the key traits of successful retail associates and develop those skills in your staff.

- Implement retail hiring and training best practices to boost performance, sales, and customer service.

- Educate your staff on suggestive selling.

Key takeaways:

- You could be losing staff productivity (and ultimately profits) to “organizational drag.”

- Prevent that by streamlining your procedures, eliminating red tape, and empowering your team to do more.

11. Get more sales from your existing customers

Multiple studies have shown that selling to existing customers is more profitable than acquiring new ones. That’s why it’s incredibly important that you don’t neglect your current customers.

Make it a point to nurture your relationships with them and continuously find ways to drive sales.

Our Bralette Club (OBC) does an excellent job here. OBC implements automated email campaigns to drive sales from customers who haven’t bought anything in a while.

OBC uses Marsello to automatically segment shoppers based on their behaviors. When a customer is considered “at risk” of not returning, OBC will automatically send a “We miss you” email containing a 15% discount.

Key takeaways:

- Remember that it’s much more cost-effective to sell to existing customers than it is to acquire new ones, so invest in customer retention.

- Use tools like Marsello to streamline and automate your customer loyalty efforts and comms, so you can regularly touch base with shoppers and drive repeat sales—and profits.

12. Leverage technology to operate efficiently

We’ve touched on the value of using the right systems to run your business throughout this article, but we truly can’t stress enough how much you’ll be able to cut costs with the right technology.

Retailers that use legacy systems could be missing out on valuable sales and customer data. They also often cost businesses more money in the long run because of third-party software subscriptions and out-of-date technology. Essentially, an outmoded POS system could be costing you.

We recommend using a POS and payments system that comes as one solution so you can operate efficiently from one platform. With this kind of system, you’ll have full visibility into all your sales channels. You’ll be able to streamline your operations, view your most successful revenue streams and optimize inventory levels.

Not only that, but a unified system gives you access to valuable data that can provide you with the insights you need to make high-level business decisions—–including where to cut costs, how to schedule more efficiently, which products to boost, and more.

For instance, you can track hourly sales, allowing you to see exactly when your store is busiest. From there, you can adjust employee hours to save money.

Lightspeed POS and Payments is a unified system for retailers who want to grow. Retail store The Brande Group saves time and money with Lightspeed.

“We needed to find a better solution so we can manage our inventory, our staff, our operation, finance and everything under one roof,” says the company’s retail buyer Guillaume de Laplante.

Ultimately when they switched to Lightspeed for their stores, they saved 50% on operational costs. This is just one example of how leveraging the right technology can improve a retailer’s profitability.

Key takeaways:

- You could be losing money by using legacy systems that don’t give you full scope of your business operations.

- Avoid that by using a POS and payments system that uses updated technology so you can operate efficiently from one platform.

13. Manage customer relationships effectively

There are many benefits to properly managing your customer relationships. Keeping customers happy at every part of their journey with your business encourages loyalty, word-of-mouth support and repeat purchases.

Here’s a list of ways you can strengthen these ties:

- Get to know your customers: understand your target audience, their preferences, buying behavior and demographics. Google Analytics is a good resource for this, as well as any customer data you have access to within your POS system.

- Personalize the customer experience: every customer is unique. You can’t appeal to everyone’s specific needs all the time, but you can tailor your marketing strategy to include targeted promotions, personalized deals and exclusive offers that align with their preferences. A customer’s sales history can help you implement these strategies.

- Excel in customer service: we mentioned this earlier, but it’s worth reiterating that friendly, knowledgeable and empathetic employees play a key role in whether a customer has a good experience at your retail store,

- Implement loyalty programs: we’ll talk more about this later, but loyalty programs can go a long way in cultivating strong relationships with your customers.

- Create channels of communication: your shoppers don’t just want to hear from you when you’re alerting them of deals—–they need to be able to get in touch with you via clear and consistent communication channels.

- Seek feedback: businesses that genuinely care about their customers will seek their feedback in surveys, reviews and over social media.

- Anticipate customer needs: retailers can benefit from proactively identifying customer needs. Stay ahead of trends and change up your product offerings to better serve customers.

- Create a community: social media plays a big role for many brands these days. It’s important to post on social channels and encourage user-generated content.

Key takeaways:

- Don’t downplay the importance of your customer relationships.

- There are many ways to foster strong loyalty, including knowing your customer base inside and out, offering personalized deals and strong customer service.

14. Maximize online sales opportunities

Make sure your website is optimized for users. Ensure your site is visually appealing, easy to navigate, has high-quality product images and a simple checkout process. If you think your online store could be better, conduct a visual audit and take steps to improve it.

Next, focus on search engine optimization: this way, you can improve your site’s visibility in search engine results, leading to higher traffic. Use relevant (and accurate) key words, tags and product descriptions.

You can also offer online-only sales to incentivize customers to make online purchases. Consider limited-time offers and loyalty discounts, which you can send customers via email.

One of the main uses of AI to boost online sales is product recommendations. AI-driven engines can suggest products based on what’s in a customer’s cart or their past purchases and preferences. This can increase cross-selling opportunities.

Another way to reduce abandoned carts is a strong checkout flow. When buyers are redirected to third-parties to make a payment, that automatically decreases distrust. Further, a slow or confusing checkout can frustrate customers and cause them to doubt the security and integrity of your website.

In fact, according to Statista, 19% of US consumers abandon their orders at checkout due to not trusting a site with their credit card information and 18% because the checkout process was too long or complicated.

Here are a few other things to consider if you want to boost online sales:

- Consider enabling live chat to help customers while they shop

- Regularly analyze data analytics and customer data to identify areas for improvement (you can access data in your POS system as well as through tools like Google Analytics)

- Showcase customer reviews and testimonials on your site

Key takeaways:

- By implementing just a few measures, you can increase your website traffic and keep customers coming back.

- Optimizing your website for users, maximizing SEO and using a good payment processor can all help drive sales.

15. Practice sustainability for long-term profitability

It’s important to consider your business’s environmental and ethical impact. Implementing sustainable practices wherever possible benefits your customers and the world around you. Sustainability can also contribute to profit in the long run.

One place to start is in your supply chain. Seek partnerships with suppliers who prioritize eco-friendly practices as well as ethical sourcing and fair labor practices. You can also manage the life cycle of your products—consider the impact of the materials, production and packaging processes you use. Even just using products without unnecessary packaging, or with recyclable packaging, creates less waste and can attract environmentally conscious customers.

At your retail stores, invest in energy-efficient lighting, heating and cooling systems. This will help you lower utility costs and reduce your carbon footprint. Plus, go further and adopt waste-reduction strategies. Minimize packaging, encourage recycling and don’t make unnecessary purchases.

Key takeaways:

- By improving your business’s sustainability standards, you’ll contribute to long-term profitability.

- Even the smallest measures, like minimizing waste at your store, make a difference. Do what you can to reduce your environmental impact, and cut costs in the process.

16. Analyze market trends to make strategic decisions

You can boost retail profit margins by analyzing the market. You should always stay informed about industry trends. Regularly follow news and updates about your industry and competitors. This will help you understand emerging trends, shifts in consumer behavior and tech advancements that may impact your sector.

By better understanding new market trends and changes in consumer behavior (for instance: are consumers buying less in a particular sector?) you can adjust your offerings accordingly, both online and in-store. By tapping into customer behavior, you can serve them better and make more sales as a result.

Another way you can do this is by gathering market research through focus groups, surveys and data analytics to gather insights into customer preferences and market demands. Plus with the customer data you have at your disposal within your POS and payments system, you can analyze how customers shop at your store compared with larger market trends.

You should also analyze your competitors. Understand their strategies, evaluate strengths and weaknesses, and figure out how to differentiate your brand from the competition to attract customers.

Key takeaways:

- Conduct market research to stay on top of emerging trends and customer preferences. This allows you to be more proactive when adjusting your product offerings to better meet customer needs.

- Analyze your competitors and stay informed about your industry.

17. Train and motivate employees

Employees are the heart of your business. That’s why it’s so important to properly train and motivate your employees. Doing so will help not only the employees themselves thrive but also boost your profitability.

Every employee you train is an investment, so try to ensure your business has a low turnover rate. It’s no surprise that the retail industry has such a high employee turnover rate, at around 60% across the US for several years now. Sure, the industry provides a lot of short-term jobs for people, but that’s not the only reason turnover is so high. Sadly, many people feel overworked and underpaid in retail jobs.

Think about it: a poorly trained employee who feels unappreciated, for instance, isn’t going to feel motivated at work. In fact, they’ll probably leave due to these frustrations—and as a business owner, you’ll be back to square one.

So how can you keep your turnover rate low?

- Clear onboarding process: clearly communicate your company’s values and mission and provide thorough training on products, services, retail operations and policies to set employees up for long-term success.

- Ongoing training: implement continuous training programs to refresh employees’ skills, improve product knowledge and fill any gaps.

- Performance feedback and recognition: implement a two-way system for feedback (where employees can also provide feedback) and recognize hard work and achievements to boost morale and performance.

- Set goals and long-term plans: work with employees to develop personalized plans for professional growth—this will help with employee longevity.

- Cross-training: give employees the opportunity to learn other roles if they’d like, which enhances their skill set and encourages teamwork.

- Effective communication: make sure you foster an environment of professional and open communication among employees, management and other teams.

All of these measures can help you retain employees. By investing in employee training, they’ll be better equipped to sell products and help customers. Remember that customers will remember a positive experience with your employees and will be more likely to return to your business.

Key takeaways:

- Invest in training your employees thoroughly so they stay with your business longer.

- When your employees know the ins and outs of your operation, they’ll be able to sell better and create better customer experiences.

18. Optimize store layout and design

Have you ever walked into a store, immediately disliked its setup or design, and felt much less inclined to shop there? We’ve probably all had this experience.

In other words, the way your store is laid out and designed can significantly impact your sales. There are several strategies you can use to make your store stand out from competitors in a good way and encourage foot traffic, including:

- Considering the customer’s journey the moment they enter your store to checkout in order to ensure that this layout provides the ultimate shopping experience

- Strategically placing high-margin and popular products in prime spots around your store so you can maximize sales

- Use attractive and cohesive displays that attract customers and encourage them to purchase more products

- Clearly categorize products so customers can easily find what they are looking for

- Train staff to be knowledgeable and approachable—this can make all the difference is whether a customer decides to make a purchase

- Use technology, such as digital displays and interactive kiosks, to enhance the shopping experience

- Experiment with store layouts, product placements and displays and analyze customer preferences

- Ensure your store is accessible to all customers

By implementing these measures, you can increase foot traffic and ultimately make more sales. A strong store design paired with good customer service can attract customers, encourage more purchases and keep people coming back.

Key takeaways:

- Don’t underestimate the impact of your store layout on customers’ purchasing decisions.

- Consider all the ways you can improve your store layout to encourage more foot traffic, including strategic product placement and experimenting with different layouts.

19. Implement loyalty programs and incentives

Loyalty programs reward customers and encourage repeat business. By helping your most loyal customers, they’re more likely to not only continue to support your business, but also recommend you to others.

Before implementing a loyalty program, make sure you really understand your customers, their preferences and purchasing patterns. You can use this information to ensure the program is high-impact.

Ensure the program’s structure is simple and straightforward. People can lose interest fast when reading something on your site or in an email. Customers should be able to easily understand how the program works, the benefits they will receive, and how they can earn and redeem rewards.

Use a tiered rewards system to keep members. Increasing levels of membership can incentivize customers to reach higher spending thresholds, encouraging them to become more loyal to the brand over time. You can also offer different rewards when customers are shopping online vs. in-store.

Key takeaway:

- Loyalty programs are a great way to retain your repeat customers and encourage more future sales.

20. Sell across all channels

Over the last few years, social commerce has boomed as an industry. Businesses of all sizes and types are selling across all social media platforms, from Instagram to Facebook to TikTok. In fact, last year social commerce sales in the US reached nearly $65 billion and it’s only expected to keep growing.

Platforms like Instagram Shop and TikTok Shop make it easier than ever for businesses to widen their market reach and boost revenue streams. If you haven’t already started selling on these channels, consider strengthening your online presence and sales by doing so.

Check out what your competitors are doing. Are they selling across these platforms? If so, it may be time for you to jump into this space, where the opportunities for selling are endless. Of course, there’s a lot more competition on these platforms, so you have to find ways to market your brand to make it stand out.

Part of this involves boosting your overall social media presence and following, which takes time, but can do a lot for your business’s sales in the long run. Targeted ads, consistent posting and working with social creators are just a few of the ways you can market your brand effectively in the digital space.

Key takeaways:

- It may be time to sell on social media platforms if you aren’t already.

- Market your brand effectively to boost your online presence and increase digital traffic.

Take action to increase your profit margins

Although the tactics you use to increase your store’s net profit margin will vary depending on your sector and what type of product or service you sell, several things are constant across all types of retail businesses:

- Selling online is an excellent way to generate more sales and costs less than opening a second retail location.

- Avoiding markdowns and discounts by improving your inventory purchasing will help maximize each item’s gross profit.

- Purchasing seasonal inventory in advance may reduce its COGS and increase your gross profit.

- Reducing operational expenses will result in you having more liquid capital to invest elsewhere. Just make sure you aren’t sacrificing the customer experience as a result.

- Leverage technology to run your business and get valuable, actionable insights on your customers and sales.

- Look for ways to increase in-store sales and your customers’ ATV.

Ultimately, each of these tactics has a similar objective: spending less and selling more. As you prep your retail store for long-term growth, consider applying them in your day-to-day operations and monitor their impact on your bottom line.

If you’re looking for a POS and payments system that can provide you with the tools you need to grow your business, talk to a Lightspeed expert today.

FAQ

1. What are typical retailer margins?

Retailer margins vary by industry but typically range from 5% to 30%, with grocery and electronics having lower margins and luxury goods having higher margins.

2. What is the retail margin rate?

The retail margin rate is the percentage difference between the cost of goods sold (COGS) and the selling price. Rates can range widely, but a common average is around 50%.

3. What retail store has the highest profit margin?

Luxury goods and high-end fashion retail stores often have the highest profit margins due to brand premium and exclusivity.

4. What is a good markup for retail?

A standard retail markup is often 50%, meaning the selling price is 150% of the cost. However, markups vary by industry and business strategy.

5. What’s a good profit margin for a small business?

A good profit margin for a small business depends on the industry but is generally considered strong if it falls within the range of 10% to 20%.

6. What is a good profit margin for online retail?

A good profit margin for online retail varies but is often in the range of 15% to 30%. Efficient operations and low overhead costs contribute to higher margins.

7. What type of retail store is most profitable?

The most profitable type of retail store can vary, but specialty stores with unique, high-margin products or services often have higher profitability.

8. What type of retail store makes the most money?

Luxury goods stores, followed by specialty stores and niche markets, tend to make the most money due to higher profit margins and exclusivity.

News you care about. Tips you can use.

Everything your business needs to grow, delivered straight to your inbox.